Why Your Dental Insurance Is Designed to Fail You (And What to Do About It)

You pay your premium every month. You picked a plan with “dental coverage.” So why does the bill still shock you?

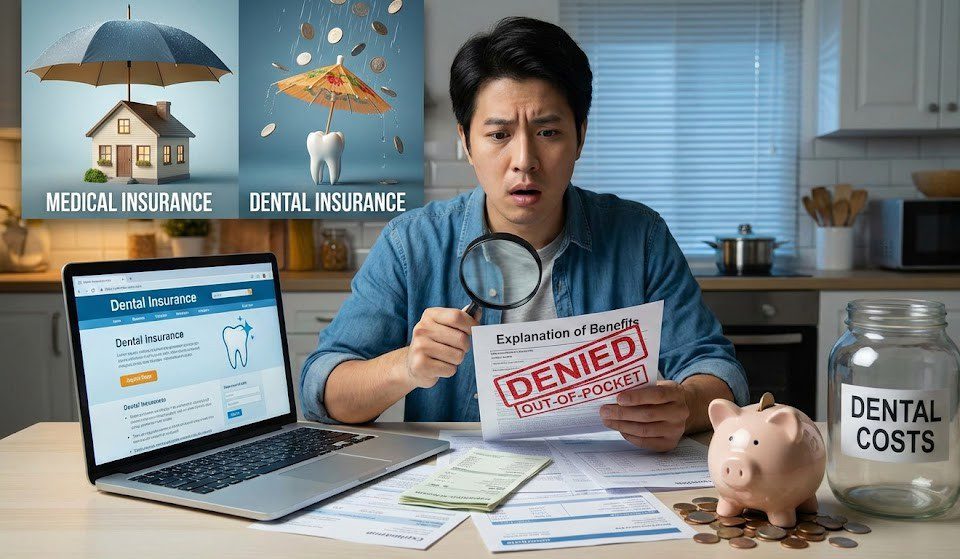

You are not alone. Dental insurance works differently than medical insurance. And once you understand how, the frustration starts to make sense.

Dental Insurance Is Not Really Insurance

Medical insurance protects you from big costs. If you need surgery, your plan covers most of it. That is the whole point.

Dental insurance does not work this way.

Most dental plans cap your annual benefits between $1,000 and $1,500. That number has barely changed since the 1970s. Back then, $1,000 could cover a lot. Today, a single crown can cost $800 to $1,500. One root canal and crown combo can wipe out your entire yearly benefit.

This is not a bug. It is how dental plans are built.

The Numbers Tell the Story

The gap between what people need and what they have is huge.

According to CareQuest Institute, 68.5 million adults in the United States do not have dental insurance. That is roughly 27% of the adult population. Nearly one in three people have no coverage at all.

But having insurance does not mean you can afford care either.

A 2024 Commonwealth Fund survey found that 41% of adults delayed or skipped dental care because of cost. This includes people with insurance. Among those who were “underinsured,” 57% avoided care they needed because they could not afford it.

The American Dental Association reports that 22.8% of working-age adults (19 to 64) had no dental coverage in 2021. Compare that to medical insurance, where the uninsured rate is around 10%. Dental coverage gaps are more than twice as common.

Why the System Works Against You

Dental plans use several tools that limit what they pay. Once you know them, you can plan around them.

Annual Maximums

Most plans pay between $1,000 and $1,500 per year. After that, you pay 100% out of pocket. If you need a crown, an implant, or multiple fillings, you can hit that cap fast.

Waiting Periods

Many plans make you wait 6 to 12 months before they cover major work. Need a crown right after signing up? You might pay full price.

Missing Tooth Clauses

Some plans refuse to cover replacement of teeth that were missing before you enrolled. Lost a tooth five years ago? Your new plan may not help you fix it.

Frequency Limits

Plans often limit cleanings to two per year and X-rays to once every 12 to 24 months. If your dentist recommends more frequent care, you pay the difference.

Downcoding

Insurance companies sometimes pay for a cheaper procedure than the one you received. Your dentist placed a tooth-colored filling. The plan pays for a silver one. You cover the gap.

Who Gets Hurt Most

The insurance gap hits some groups harder than others.

Adults over 65 face the biggest challenge. Only 29.2% of elderly Americans have dental benefits, according to CDC data. Medicare does not include dental coverage. Millions of seniors must choose between paying out of pocket or skipping care.

Low-income families struggle too. CareQuest found that adults with lower incomes were far more likely to report cost as a barrier to seeing a dentist. When money is tight, dental care often gets cut first.

The result shows up in emergency rooms. When people cannot afford preventive care, small problems become big ones. Infections spread. Pain gets worse. And the only option left is the ER, which costs more and often cannot provide real treatment.

What You Can Actually Do

Knowing the system helps you work around it.

Use Your Benefits Before You Lose Them

Most plans reset on January 1. If you have remaining benefits in November, use them. Schedule that cleaning or get that filling done before your cap resets to zero.

Ask About Treatment Timing

If you need work that exceeds your annual max, ask your dentist about splitting it across two plan years. Get the first crown in December. Get the second in January. Two caps instead of one.

Get a Pre-Treatment Estimate

Before any major work, ask your dental office to submit a pre-authorization. This tells you what the insurance will pay before you commit. No surprises.

Compare the True Cost

Sometimes paying out of pocket costs less than you think. Many dental offices offer payment plans or discounts for patients without insurance. Ask about your options.

Look Into Dental Savings Plans

These are not insurance. They are discount programs. You pay an annual fee and get reduced rates at participating dentists. For people without coverage, this can cut costs by 10% to 60%.

Prevention Pays Off

The best way to beat the system is to need less major work.

Regular cleanings catch problems early. A small cavity costs far less to fix than a root canal. Gum disease caught early can be reversed. Caught late, it leads to tooth loss.

The American Dental Association recommends preventive visits at least once a year. Many dentists suggest twice. These visits often fall within your plan’s coverage with little or no out-of-pocket cost.

Prevention is the one area where dental insurance actually works in your favor. Use it.

The Bigger Picture

Dental insurance was never designed to cover everything. It was designed to help with routine care and offset some costs. Understanding that difference changes how you plan.

You would not expect car insurance to pay for oil changes. Dental insurance is closer to that model than it is to medical insurance. It helps with maintenance. It chips in on repairs. But it will not cover a full rebuild.

Once you accept that reality, you can make smarter choices. Budget for out-of-pocket costs. Use your benefits strategically. Prioritize prevention.

Your teeth are worth the investment. The insurance company is not going to make that investment for you.